MUST READ: Fed Admits Crony Truth About Pandemic QE: “it creates new bank deposits”

This is a very important explanation of how a privately owned central bank is waging an economic war on We the People. The “pandemic” Quantitive Easing (QE) operations of the Fed were designed to enrich the very criminals behind the PSYOP-19 depopulation and control program while simultaneously and most premeditatedly ushering in PSYOP-HYPERINFLATION.

This substack has previously pointed out that the Fed funds most of the scientific publications in America. That is beyond a conflict of interest.

As you read the below article think about what other criminal entities the Fed could also easily be funding through its asset books, entities like the unconstitutional agencies the CIA, FBI, FDA, CDC, etc. Then think about how the Fed could fund the criminal IRS which only exists to social engineer We the People into impoverished compliance and quite literally premature death. One could easily make the argument that the Fed exists to social engineer Main Street while stripping all of the private property of America.

Now consider the possibility that the Fed has shadow asset books and what those conjured out of thin air dollars could also be funding and which entities could be enriched…

And the Fed is perfectly aligned with the WEF and UN agenda of One World Government hell on earth, as evidenced by not only its sordid history, but also by its telegraphed and inevitable rollout of its “vax” passport social credit score tethered CBDC.

The below article must be appreciated in terms of the 4th Industrial Revolution context, with technocommunist corporations like BlackRock and Vanguard pushing extremely hard now with literal blackmail terms for PSYOP-CLIMATE-CHANGE compliance across the entire business sector in order to control all of America, and then the entire planet itself.

by John Titus

New video is up.

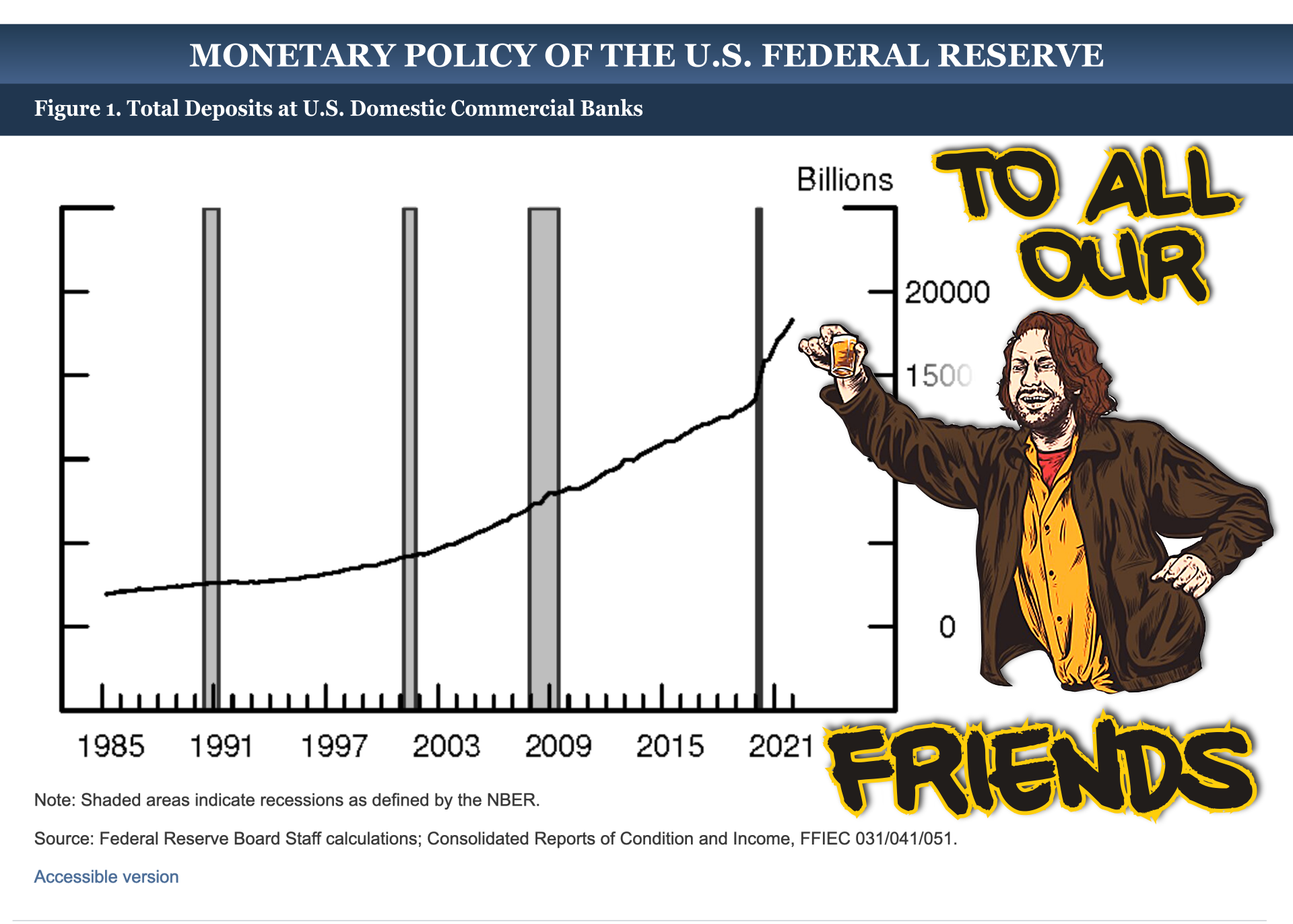

I have made four BestEvidence videos that drive home the same essential point about the Fed’s asset purchase program (QE) under cover of “PANDEMIC!!!”—namely, that it radically departed from previous iterations of QE by creating new bank deposits. The core thesis of those videos, denied by media financial punditry, has now been validated by the Federal Reserve itself, in a research note dated June 3, 2022.

Thanks for reading BestEvidence! Subscribe for free to receive new posts and support my work.

✓

What’s so interesting about this is WHERE those new bank deposits have appeared, because it tells you everything you need to know about the true remit of the Federal Reserve, which, to the surprise of no one paying attention, is to enrich its owners at the direct expense of the rest of us.

Let’s take these two basic points in turn, as this video does.

Pandemic QE directly fueled the creation $4 trillion in new retail bank deposits

For the record, the BestEvidence videos discussing this basic point are as follows:

1. Quantitative Easing Is the Biggest Sham Ever (Dec. 17, 2020)

2. Larry & Carstens' Excellent Pandemic (Aug. 14, 2021)

3. Meet the Fed's New BFF (Nov. 24, 2021)

4. Toilet-flushing the U.S. in 3 Exciting Fed Colors (June 29, 2022; i.e., after the Fed research note)

It’s no small affair, these newly Fed-funded bank deposits. No, we’re talking about trillions of new dollars that have flooded the U.S. pool of retail bank deposits, thanks to what the Fed did under cover of “PANDEMIC!!!” In fact this is where your inflation comes from, as shown in “Toilet-flushing the U.S. in 3 Exciting Fed Colors”

Despite the empirical reality of the Fed’s pandemic QE actions, and the inflation it’s caused, a phalanx of financial gurus descended like locusts across all media over the last two years, all denying that it’s even possible for QE to effect the creation of new bank deposits. These pundits, despite bearing every political stripe imaginable, curiously offer exactly the same empty sloganeering in their evidence-free rush to make one basic Fed-apologizing point: “QE is just an asset swap,” “reserves don’t leak out into the banking system,” “QE isn’t inflationary”, “QE is merely a balance sheet operation” etc. etc. According to these gurus, QE could not have any direct effect on bank deposits. NOT. POSSIBLE. At least not according to the financial experts.

Until recently, there was no referee in sight to declare a winner in this $4.5 trillion dispute, which featured a united front of financial pundits in one corner and in the other corner your lone YouTube leper, to wit, BestEvidence. The lack of any referee aside, it’s actually pretty hard to discover that there’s a debate at all given the media’s presentation of only one side—the Fed’s side—of the equation: QE doesn’t affect ordinary bank deposits, didn’t ya know?

But alas there has been such a debate, and now there’s a ref to go with it, and a winner as well. But let’s talk about the loser first, because it’s so much more interesting. And that loser is the united financial punditry. Who could’ve guessed?

Yes, it’s true: some two-plus years after the Fed launched an avalanche of PANDEMIC!!! QE programs, a referee entered the ring at last, in June of this year (2022), to decide the match. That ref, as fate would have it, is none other than the Federal Reserve itself, speaking through researchers. And the winner—by data-packed knockout—is BestEvidence.

Here is five-word holding of the Fed itself: “it creates new bank deposits.”

“It” means asset purchases by the Federal Reserve where the asset being purchased comes from a non-bank.

You see, that’s how QE during “PANDEMIC!!!” (let’s call it PAN-QE) worked—the Fed bought assets from non-banks. QE during the global financial crisis (GFC-QE) wasn’t done that way.

Specifically, GFC-QE was a bailout of the banks, whereas PAN-QE was a transparent sop to non-bank financial institutions like BlackRock. That difference, perhaps seemingly minor (does it really matter if trillions of freshly created dollars flow into the coffers of Citigroup or BlackRock?), in fact had implications every bit as large the $4.5 trillion expansion of the Fed’s balance sheet under PAN-QE.

Using graphs from the Fed’s own FRED website, together with visual demonstrations of what happens, mechanically, when the Fed buys an asset from a non-bank, these BestEvidence videos demonstrated that U.S. bank deposits increased in lockstep with the Fed’s balance sheet. That’s because for every new dollar created by the Fed to buy something from a non-bank, somewhere there’s a commercial bank that has to create a new deposit account dollar in order to make that purchase happen.

The reasons for this are as byzantine as our debt-based monetary system, which is why I made these videos to begin, but the bottom line is this: PAN-QE is inherently inflationary because it necessarily adds to the pool of bank deposits in the U.S.—and GFC-QE wasn’t, because the mechanics of a Fed asset purchase from a bank are a simple two-party asset swap, basically. That’s glaringly apparent from the Fed’s graphs.

It is now 30 months since the Fed’s hysterical cold-and-sniffles money-printing operation began, and yet to this day I still see self-appointed financial experts and gurus on TV and in videos assuring viewers that QE is not inflationary because (pick your snake oil) “reserves don’t leak out into the banking system,” “it’s just an asset swap,” “reserves are inert,” “it’s a balance sheet neutral operation,” etc.—all wrong, wrong, wrong and wrong.

I’d pretty much given up my quixotic battle for monetary clarity when I stumbled across a June 2022 research note from the Federal Reserve itself. I’m pretty sure I got it from the comment section of a Mish blog post, but I couldn’t tell you which one.

Anyhow, the “debate” (really, the denial) is over: the Fed can directly effect the creation of new bank deposits by buying assets from non-banks.

Implications of the Fed-fueled new bank deposits

You might think, as was my initial inclination, that the vast heft of new QE-fueled bank deposits is sitting in institutional bank accounts, what with continent-sized evil doers, er, asset managers like BlackRock plundering the assets of the earth.

That’s true, yes, to a significant degree. But even more of the deposits are sitting in household accounts. And that’s a very interesting thing, for a couple of reasons.

One, you might think, thanks again to financial pundits, that those accounts belong to the bottom 50% or 90% (by wealth) of households, thanks to the pandemic stimulus programs of the federal government. But that’s not the case: the new deposits mimic the wealth distribution curve itself, meaning (as seemingly always) the rich got richer and the poor got, well, marginally richer in nominal terms before you factor in inflation and… oh, yes, the poor got poorer.

But regardless of how the newly created deposits were skewed wealth-wise, more interesting is what the appearance of those deposits across all bands of wealth tell us about the Federal Reserve: it can fund whoever the hell it wants to, when it wants to. Meaning this: the Federal Reserve could’ve funded retail bank accounts in the wake of the global financial crisis too.

It just didn’t want to. It bailed out criminal banks, its owners, which then turned around and fraudulently foreclosed on millions of underwater homeowners, whom the Fed could’ve helped out but didn’t because that wasn’t what the Fed wanted. It wanted foreclosures, even if it meant stealing people’s houses, which is exactly what the Fed got.

Are you starting to get at least an inkling that a central bank digital currency might be bad news for you and hundreds of millions or really billions of other people? God, I hope so.

—John Titus

Do NOT comply.

Follow the money. 💰when bill gates was interviewed right at the very beginning of this

Scam pandemic he said “yes there will financial

Hardship” and gave his awkward laugh. So am I getting this correct? So basically by weaponizing a virus vaxxine which businesses

Win the big money changers seize assets enriching themselves as people lose jobs health

Homes and maybe that’s too basic …1913

The Federal Reserve becomes the private banking cartel of the USA … and these fuckers

Weaponize money 💰 and all the financial experts are like the medical experts which lie

Cheat steal kill for influence power supporting

An agenda that crushes everyone who’s not

Part of their club. All the while mocking us

Hmmmm not acceptable. You have made my

Fathers house a den of thieves.

"...the Fed is perfectly aligned with the WEF and UN agenda..."

Banker Paul Warburg, the "architect of the Fed", was a founding director of the Council on Foreign Relations (CFR), and nearly every Fed chair since WW2 has been a CFR member. Current Fed chair (Powell), vice-chair (Brainard), and Treasury secretary (Yellen) are long-time CFR members.

CFR members were also the architects of the UN organization. CFR members, including Kissinger, helped launch the WEF.

BlackRock "partners" with the Fed. Larry Fink is a CFR director and a WEF trustee. Carlyle Group founder David Rubenstein is the CFR chair and a WEF trustee. Fed chair Powell is a former Carlyle partner.

They're all nodes in an interlocking network, working towards the same goal.