REPOST: Memorandum of Law: The Legality Of Income Taxation In The "50 States" Of The Union

“Nemo agit in seipsum.”

No man acts against himself.

Following his resignation, T. Coleman Andrews, who served as IRS Commissioner for nearly 3 years during the early 1950s, made the following statement:

Congress [in implementing the Sixteenth Amendment] went beyond merely enacting an income tax law and repealed Article IV of the Bill of Rights [the 4th Amendment], by empowering the tax collector to do the very things from which that article says we were to be secure. It opened up our homes, our papers and our effects to the prying eyes of government agents and set the stage for searches of our books and vaults and for inquiries into our private affairs whenever the tax men might decide, even though there might not be any justification beyond mere cynical suspicion.

The income tax is bad because it has robbed you and me of the guarantee of privacy and the respect for our property that were given to us in Article IV of the Bill of Rights. This invasion is absolute and complete as far as the amount of tax that can be assessed is concerned. Please remember that under the Sixteenth Amendment, Congress can take 100% of our income anytime it wants to. As a matter of fact, right now it is imposing a tax as high as 91%. This is downright confiscation and cannot be defended on any other grounds.

The income tax is bad because it was conceived in class hatred, is an instrument of vengeance and plays right into the hands of the communists. It employs the vicious communist principle of taking from each according to his accumulation of the fruits of his labor and giving to others according to their needs, regardless of whether those needs are the result of indolence or lack of pride, self-respect, personal dignity or other attributes of men.

The income tax is fulfilling the Marxist prophecy that the surest way to destroy a capitalist society is by steeply graduated taxes on income and heavy levies upon the estates of people when they die.

As matters now stand, if our children make the most of their capabilities and training, they will have to give most of it to the tax collector and so become slaves of the government. People cannot pull themselves up by the bootstraps anymore because the tax collector gets the boots and the straps as well.

The income tax is bad because it is oppressive to all and discriminates particularly against those people who prove themselves most adept at keeping the wheels of business turning and creating maximum employment and a high standard of living for their fellow men.

I believe that a better way to raise revenue not only can be found but must be found because I am convinced that the present system is leading us right back to the very tyranny from which those, who established this land of freedom, risked their lives, their fortunes and their sacred honor to forever free themselves...

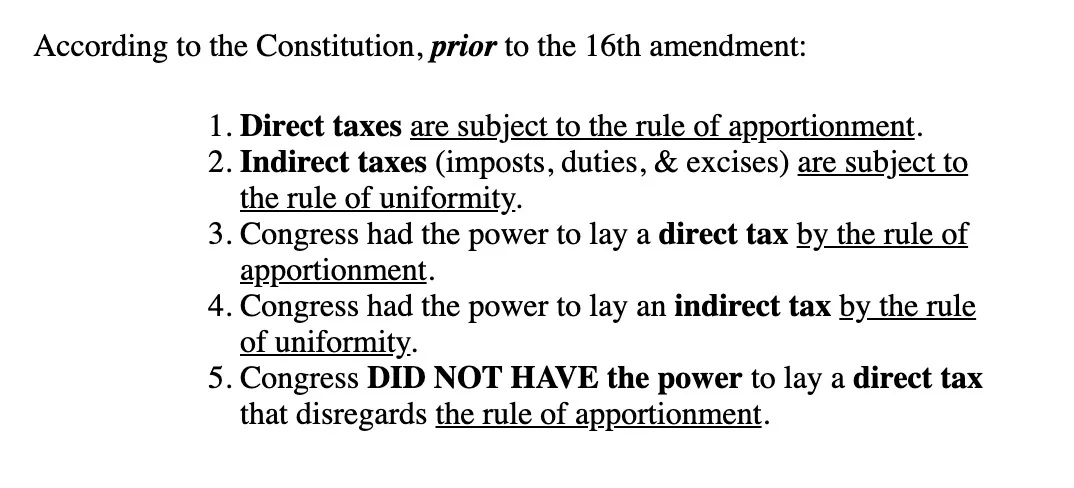

The Federal income tax also happens to be wholly unconstitutional and as such unlawful to forcefully impose, which is precisely why the IRS engages in legal trickery when stealing from We the People.

Under color of law, blatant fraud, and ignorance of law, the unconstitutional imposition of direct and un-apportioned taxation (i.e. “income” taxes) was foisted upon We the People.

This is not “anti-government” conspiracy theory; this is legal fact.

The illegitimate Federal government operating out of the foreign nation of Washington, D.C. is waging a full spectrum soft-war against its citizenry, actively diminishing its subjects by threat of violence through counterfeit laws, with taxation having always been an especially potent control knob.

This substack has previously exposed taxation as illicit social engineering through the “Death and Taxes” meme which paved and paid the way for other criminal ideological State programming and democide, such as “Trust the Science:”

Since the passing of the unconstitutional, and, some would argue, unratified 16th Amendment in 1913, with the associated Title 26 U.S.C. of the Internal Revenue Code (IRC) having been complied with in 1939, Congress has been engaged in the willful subversion of its duties, legislating against the very citizenry that they pretend to represent.

The unlawful IRC is currently 3,837 pages long. The average person would be so daunted and overwhelmed to even consider perusing such an overlong and byzantine document, let alone questioning its legalities. Add in the lifelong indoctrination of “Death and Taxes” heading into each and every tax season, and we end up with a fearful, ignorant and brainwashed majority of compliant slaves.

The fact that the judicial system is also indoctrinated and captured such that they refuse to uphold the Constitution while imposing under threat of violence bogus tax laws allows for a hopelessly corrupt system that reinforces its own accelerating death spiral.

If one were to actually parse the IRC tax code, then they would realize that it is nothing more than an exercise in sleight of word, and purposely deceptive terms with the aim and intention of confounding We the People such that the residents of their respective nation States are undermining their very own best interests.

But what exactly is being paid in these “income” taxes, and to whom?

Nature of Federal income tax.

56. Every payment of Federal income tax is classified as a gift and 100% of all collections of income tax are used by the Secretary of the Treasury to make payments of interest on the debt owed by the Federal government to the private Federal Reserve Bank; to wit:

(1) The Secretary of the Treasury may accept, hold, administer, and use gifts and bequests of property, both real and personal, for the purpose of aiding or facilitating the work of the Department of the Treasury. . . .

(2) For purposes of the Federal income, estate, and gift taxes, property accepted under paragraph (1) shall be considered as a gift or bequest to or for the use of the United States. Title 31 U.S.C. § 321(d).

BEQUEST. A gift by will of personal property. [p. 339] . . . GIFT. . . . A voluntary, immediate, and absolute transfer of property without consideration. . . . [p. 1352] BOUVIER’S, pp. 339 and 1352, respectively.

Resistance to additional income taxes would be even more widespread if people were aware that . . . 100 percent of what is collected is absorbed solely by interest on the Federal debt . . . In other words, all individual income tax revenues are gone before one nickel is spent on the services which taxpayers expect from their Government. J. Peter Grace, “President's Private Sector Survey on Cost Control: A Report to the President,” Vol. I, January 12, 1984, p. 3.

The Federal Reserve is not an agency of government. It is a private banking monopoly. . . . [T]he policies of the monarch are always those of his creditors. Rep. John R. Rarick, “Deficit Financing,” Congressional Record (House of Representatives), 92nd Congress, First Session, Vol. 117—Part 1, February 1, 1971, pp. 1260-1261.

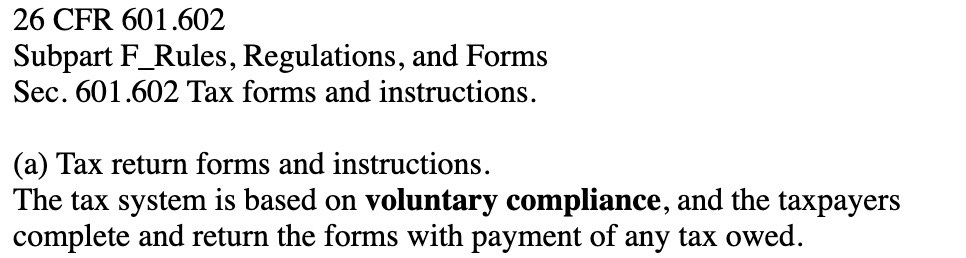

A gift is by definition voluntary, and this is further corroborated in the actual tax return forms; to wit:

Therefore, income taxes are gifts to a privately owned central bank that funds the very inflation (stealth tax) that it purposely generates through monetary policies, which in turn serves to enrich their private owners at the expense of the increasingly impoverished populace.

The Federal government continually accrues ever greater debt owed to said private bank, which in turn is ultimately owed by We the People.

The Treasury and its IRS run cover for both the Fed and Congress. The secondary benefit of this scheme is that theft of “disposable income” through taxation also serves to increase the propensity to borrow from those very same Fed owners; namely, the banksters, and, ultimately, the dynastic banking families at the very top of this One World Government pyramid.

What we then have is a disguised neo-feudal model, with “capitalism” as merely a cosmetic term for today’s crony capitalism, which is essentially a more advanced technocratic communism 2.0, or technocommunism.

This tyranny can only be made possible by a captured Congress ceding one of its most critical functions:

"The Congress shall have power ... to coin money, regulate the value thereof, and of foreign coin, and fix the standard of weights and measures."

But are Americans then in fact responsible for this “voluntarily” income tax filing for these exorbitant “gifts” to the Federal government?

Code of Federal Regulations: only D.C. residents liable to tax under Title 26 U.S.C.

44. The correctness of our interpretation of the meaning of “State” (supra, paragraph 39), that the only body politic liable to tax under 26 U.S.C. is that of the District of Columbia, is confirmed in pertinent part of general legislation in Title 26 C.F.R. Internal Revenue; to wit:

§ 1.1-1 Income tax on individuals.

(a) General rule. (1) Section 1 of the Code imposes an income tax on the income of every individual who is a citizen or resident of the [Title 26 U.S.C. geographical] United States [i.e., District of Columbia only] . . .

(b) Citizens or residents of the [Title 26 U.S.C. geographical] United States [i.e., District of Columbia only] liable to tax. . . .

(c) Who is a citizen. Every person born or naturalized in the [Title 26 U.S.C. geographical] United States [i.e., District of Columbia only] and subject to its [the District of Columbia’s] jurisdiction is a citizen. . . .

45. Whereas: Only citizens or residents of the Title 26 U.S.C. geographical United States are liable to tax under Title 26 U.S.C. (26 C.F.R. 1.1-1(b)); and

Whereas: Persons born or naturalized in the Title 26 U.S.C. geographical United States nevertheless are not citizens thereof unless they are also subject to Title 26 U.S.C. geographical United States jurisdiction, i.e., unless they are also a resident thereof (26 C.F.R. 1.1-1(c)); to wit:

RESIDENT. One who has his residence in a place. BLACK’S, p. 1032. RESIDENCE. Living or dwelling in a certain place permanently or for a considerable length of time.

The place where a man makes his home, or where he dwells permanently or for an extended period of time.

. . . “Residence” means a fixed and permanent abode or dwelling-place for the time being, as contradistinguished from a mere temporary locality of existence. . . . Id.

—Territorial jurisdiction. Jurisdiction considered as limited to cases arising or persons residing within a defined territory, as a county, a judicial district, etc. The authority of any court is limited by the boundaries thus fixed. . . . [Underline emphasis added.] Henry Campbell Black, A Law Dictionary, Second Edition (West Publishing Co.: St. Paul, Minn., 1910), p. 673.

Whereas: For purposes of income tax under Title 26 U.S.C., it is immaterial if one was born or naturalized in the Title 26 U.S.C. geographical United States if he does not reside in the Title 26 U.S.C. State of District of Columbia (see paragraph 39, supra), i.e., is not a resident thereof,

Wherefore: The only persons who are liable to tax under the Internal Revenue Code / Title 26 U.S.C. are residents of the District of Columbia.

As per the actual code, only residents of the District of Columbia are required to pay taxes, and, by extension, Federal government employees.

So then how can the IRS lay claim on all 50 States of the union, if the District of Columbia is only one “State” which by law is not part of the union, and as such is a de facto foreign nation operating with an exceedingly narrow set of powers within the collection of the united States of America?

Meaning of the term “State” in 26 U.S.C. 6103(b)(5)(A)(i).

53. The meaning of the definition of the term “State” in 26 U.S.C. 6103(b)(5)(A)(i) comprehends the (a) (purported) 50 bodies politic of the District of Columbia residing without the exterior limits of the District of Columbia (supra, paragraph 52), (b) the body politic of the District of Columbia residing within the exterior limits of the District of Columbia, and (c) the body politic of the Commonwealth of Puerto Rico, the Virgin Islands, Guam, American Samoa, and the Commonwealth of the Northern Mariana Islands.

Meaning of the Title 26 U.S.C. term “State”.

54. The meaning of the controlling Title 26 U.S.C. definition of “State” in Section 7701(a)(10) thereof— which provides “The term ‘State’ shall be construed to include the District of Columbia, where such construction is necessary to carry out provisions of this title”—is identical to that of 26 U.S.C. 6103(b)(5)(A)(i), supra, paragraph 53.

Meaning of the Title 26 U.S.C. term “United States”.

55. The meaning of the controlling Title 26 U.S.C. definition of “United States” in Section 7701(a)(9) thereof—which provides “The term ‘United States’ when used in a geographical sense includes only the States and the District of Columbia”—is the collective of the geographic area occupied by the District of Columbia, the Commonwealth of Puerto Rico, the Virgin Islands, Guam, American Samoa, and the Commonwealth of the Northern Mariana Islands and no other thing.

Therefore, only in the act of filing an “income” tax form from outside of the geographical location of the District of Columbia does one then choose to voluntarily opt-in as a resident of the District of Columbia, while physically residing outside its territory.

By volunteering to become a resident of the District of Columbia when one’s legal status is as a nonresident alien, one thus participates in and comprises the District of Columbia as the body politic residing within the 50 States.

When citizens from within the 50 States, ignorant of the purposely misrepresented tax code “law” volunteer to file their “income” taxes, they are electing to create the body politic of the District of Columbia, whereby the IRS may then lay claims to have jurisdiction over them.

In other words, by filing “income” taxes you have given over your legal rights to the IRS by tacitly agreeing to become a subject of the “State” of the District of Columbia. You are in effect signing off on a legal document that is purposely designed to legally bind you to a swindle, and as such you have no further recourse by having entered into said binding contract.

The fact that IRS agents are also ignorant of the code, and are just as brainwashed as the judges and courts means that the average American believes in this scam, which further reinforces mass compliance.

But the IRS does not have any jurisdiction whatsoever to collect a cent from any nonresident alien in any of the 50 States, unless said citizens voluntarily file tax forms.

No requirement for nonresident aliens to make an income tax return.

48. The Federal Register, published by the Office of the Federal Register, National Archives and Records Administration, and the official daily publication for all rules—i.e., statutes—proposed rules, and notices of Federal agencies and organizations, as well as all presidential documents, is devoid of incorporation any requirement to make an income tax return; to wit:

Our records indicate that the Internal Revenue Service has not incorporated by reference in the Federal Register (as that term is defined in the Federal Register system) a requirement to make an income tax return. Michael L. White, Attorney, Office of the Federal Register, letter to Richard Durjak, May 16, 1994.

This is one of the most egregious examples of color of law. Any court enforcing this kind of theft is clearly breaking the law of the land.

Most, if not all judges presiding over “income” tax cases, as well as juries, are also guilty of this Constitutional and natural rights subversion.

Note how one must elect themselves in order to be legally stolen from; to wit:

How Joint Tenants in the Sovereignty “become residents” of the District of Columbia.

49. Any nonresident alien, such as a Joint Tenant in the Sovereignty, can appear—in the eyes of government—to elect (choose) to be treated as a resident of the District of Columbia by making a tax return; as provided in 26 C.F.R. Sections 1.871-1 and 1.871-4 and 26 U.S.C. 6013; to wit, respectively and in pertinent part:

[…]

50. Whereas, no nonresident alien has a duty to make a tax return, such return can be used by government as “evidence” of a “definite intention to acquire residence” in the Title 26 U.S.C. geographical United States (see 26 C.F.R. 1.871-4(a) and (c)(2)(iii), paragraph 49, supra).

Who in their right mind and with legal comprehension of the actual laws would ever elect themselves to be a willing participant in this kind of depraved arrangement?

The Framers were acutely aware of the tendency for a government to engage in this type of theft of the fruits of We the People’s labors. This to them constituted a perversion of natural rights, or God given rights, and directly limited an individual’s freedoms, property rights, privacy rights, and the very Constitutional rights that they so diligently prescribed for their Republic.

No matter how much the government steals via “income” taxes — even when the marginal tax rate for U.S. earners was 94%, its deficits are always unsustainable —the “income” tax “revenues” never have an actual direct bearing on the profligate government budgets, nor does this theft ever pay down the spiraling national debt.

The IRS is simply backstopping the Fed’s ruinous policies. And if the metastasizing government did in fact rely on “income” taxes, then why would Congress not take back from this private central bank their power to print money, and directly fund their untenable budgets, and associated money laundering black ops schemes?

If the Federal government always required “income” taxes to operate, then how was infrastructure paid for, the military funded, hospitals and firehouses built, police, firemen and schoolteachers all paid prior to the modern era “income” tax of the “temporary” Victory Tax by the Revenue Act of 1942? That wartime “income” tax was incidentally repealed two years later in 1944, but the citizenry was never informed of that, so they kept offering up their ever increasing “gifts” to this very day under threat of State violence.

Therefore, Occam’s Razor tells us that “income” taxation is wholly unnecessary for a legitimate Federal government. It then follows that taxation is used to oppress, stress, induce debt, and limit We the People in their freedoms. It is a subjugation tool and a most pernicious example of social engineering that is designed to control and deprive the populace by looting prosperity, and greatly limiting the ability to accumulate generational wealth through hard work and creativity.

The second Plank of the Communist Manifesto states:

A heavy progressive or graduated income tax.

What we have today is technocommunism, with “income” taxation a vital component of the Great Reset. After all, how does the UN, WEF, CFR, DoD, Pentagon, FDA, Bill Gates and his Rockefeller masters, and the various “nonprofits,” NGO’s et al. really get funded? Hint: the tax code, associated money laundering, government grants and various other handouts at the expense of the taxpayer that is in the direct crosshairs of a global eugenics operation. PSYOP-MUSK’s entire empire, not limited to Tesla, solely exists due to government grants, (ZEV) credits and kickbacks, while Amazon for its first two decades effectively paid zero taxes while the mom and pop shops it was dutifully putting out of business were saddled with all kinds of taxes, while mega corps like BlackRock pay token taxes amounting to tiny accounting rounding errors as they buy up the planet for pennies on the dollar off the backs of tax slaves struggling to make ends meet in no small part due to being stolen from by the State.

The 4th Industrial Revolution requires the constant destruction of wealth and freedom, which is precisely why PSYOP-CLIMATE-CHANGE is in no small part the all-encompassing and never-ending taxation scheme.

But even if one appreciates the true nature of “income” taxation, and how it does not apply to the nonresident alien, this system has been purposely designed to make it next to impossible to extricate oneself from the burdens of needlessly paying these grievous “gifts.”

Every corporation, and most businesses small and large alike, comply with this IRS scam. The IRS in turn relies on the employer to function as their compliance and entrapment agent for their employees. These employers tacitly aid and abet the IRS by withholding Federal “income” tax from their workers, thus electing them to becoming “voluntary” residents of the foreign nation “State” of the District of Columbia. This act of withholding “income” legally binds the employee to the IRS via their employer by forcing them to file their tax forms as a function of payrolls. The legal liability is thus transferred from employer to employee by the former “volunteering” the latter into a legally binding contract with the foreign nation of Washington, D.C. via the IRS.

The District of Columbia also happens to be harboring a wholly illegitimate Federal government that in turn empowers the IRS, a privately owned company incorporated in Puerto Rico, and the Federal Reserve “bank” that is not Federal nor has any reserves to continue to perpetrate their theft.

And even if one is able to successfully navigate the unwarranted imposition of these “gifts” to the Federal Reserve “bank” by way of the IRS, the government has now further escalated their weaponization of this criminal tax code by forcing companies such as eBay and Paypal to report any and all transactions exceeding $600.

Concurrently, the hard push by WEF “penetrated” nations for CBDC’s is also directly related to this social engineering taxation scheme as they ratchet up their cashless X Everything App social credit score ploy; to wit:

The very same corporations and businesses that are pushing the egregious ESG scam of today have always been volunteering their employees to gift away the fruits of their labors, while they themselves skirt most of their tax “liabilities.”

Corporations like BlackRock as well as far too many small businesses also happened to have pushed the DEATHVAX™ on their employees, with threats of job termination. Many of these tax slave employees were terminated over the “free” EUA “vaccines” and unconstitutional mandates that they themselves paid for.

The greatest irony is that now these very same taxpayers are experiencing skyrocketing all-cause mortality and a plethora of adverse events; in other words, they were forced to fund their very own demises.

If a socially engineered, miseducated, propagandized, and fearful citizenry is ignorant of the basic laws of the land, then what are the chances that they could even appreciate the concept of informed consent?

The global citizen is now a genetically modified debt-slave tax mule that is careening toward their own mass ritual bio-suicide denouement.

PSYOP-IRS has been one of the more effective means of destroying lives, freedoms and liberties.

While PSYOP-CLIMATE-CHANGE perfectly leverages all of the other psyops into a singular and permanent tax scheme global lockdown, with never-ending slow kill bioweapon injections en route to the X Everything App social credit score AI dystopia.

In this posthuman 4th Industrial Revolution, taxes will continue to play an integral part of the control apparatus. AI as set by technocratic overlords will algorithmically impose all kinds of taxes and inflation policies that will erode the UBI monies as doled out by the One World Government. And since UBI will be CBDC based, further currency programming will induce spending and behavioral patterns that the State desires, with the ultimate taxation being levied on those granted the “freedom” to be euthanized by the State. The tax on human life itself, to compliment “climate” taxes for a sustainable environment that is decarbonized (i.e. depopulated) planet.

Taxation in no small part is what got us to these horrific technocommunist crossroads in the first place. Think about all of the illegitimate Federal government agencies that were and continue to be funded by taxation — these are the very agencies tasked with destroying We the People’s natural rights and wealth under the pretense of “safety,” servitude and protection of those they are robbing and hurting.

If we continue to act against ourselves, then we continue allowing the powers that be to abuse us while siphoning our energy, creativity and life force from us.

There are far more of us than their are IRS agents and technocrats.

What can these fraudulent government agencies really do if there would be a significant minority of noncomplying tax refuseniks?

If enough people realize that they are in reality nonresident aliens of not just the foreign nation of Washington, D.C, but that they are also nonresident aliens of any and all governments that go against their natural rights, then this tyrannical system masquerading as a freedom-based Democracy will no longer be able to plunder under perpetual threat of color of law, or Sate violence.

Read the entirety of Memorandum of Law here.

They want you dead.

Do NOT comply.

I'll go one further and say that property taxes are unconstitutional as well. We pay sales tax when we purchase property and then property tax every year after, however, do you really own something that can be taken away from you if you do not pay said property taxes??????

Here in the UK Liz Truss tried to lower taxes and the central banks engineered a crisis and replaced her with the WEF puppet known as Rishi Sunak within a month. You are therefore bang on the money, taxes are now part of the banking billionaire playbook.